Just Do It

The code word for Nike’s tax system, for the billions stashed in offshore accounts, is short, memorable and delightfully onomatopoeic.

The word is swoosh.

Nike’s iconic logo, the swoosh, is almost as famous as the Coca-Cola font or Mickey Mouse’s ears, itself a symbol of capitalism and globalization. It was invented some 50 years ago by a graphic design student who crossed a check mark and an arrow to convey a sense of dynamism and swiftness. The fact that it came to symbolize Nike, however, was largely a coincidence. The company’s founders initially didn’t even like the logo, which was still in the draft stages. But the first shoe boxes needed to get to the printers – and fast – and so the swoosh, one of the greatest marketing success stories of our time, was born.

Understanding the swoosh is key to understanding how Nike, a multinational corporation, has managed to pay so little in taxes on the profits it earns. Around a decade ago, and then again a few years back, the law firm Appleby helped Nike restructure its business in ways that were good for the company but bad for tax authorities and, by extension, society at large. The result was a construct in which Nike has ultimately paid only negligible taxes on profits earned outside the United States. In some respects, the sports outfitter and its lawyers at Appleby have come up with the ultimate system for profit maximization, one that is as dynamic and swift as the Nike logo and leaves tax authorities in its dust. The Paradise Papers – in this case, internal documents from the law firm Appleby – have been instrumental in deciphering this system.

The reporting that would eventually lead to a deeper understanding of the global corporation's intricate system began in Brunnthal, on the outskirts of Munich. The place is home to a Nike Factory Store, packed to the ceiling with boxes of shoes for every sport imaginable along with rain jackets, windbreakers, tracksuits, shorts, socks and bags. There is something for everyone – in just about every color and size. And every article of clothing and gear has one thing in common: the swoosh.

A salesman retrieved a pair of bright blue Air Pegasus Racers. The shoes cost 70 euros, with much of that total remaining on Nike’s books. Experts from nongovernmental organizations say manufacturing costs for a pair of running shoes only average between 10 to 20 percent of the sale price.

The question then becomes: Where do those profits end up – and where are they taxed, assuming they are taxed at all?

The German offices of Nike Deutschland GmbH, which serve as the headquarters for the company’s operations in Germany, Austria and Switzerland, are located at Otto-Fleck-Schneise 7 in Frankfurt. For anyone familiar with the world of German sports, this address is a recognizable one: It’s right around the corner from Frankfurt’s main soccer stadium and down the street from the headquarters of the German Football Association as well that of the German Olympic Sports Confederation. One could be forgiven for thinking that all the revenues Nike generates in Germany ultimately wind up at this address, inside the modern building with the glass and steel façade. One could also be forgiven for thinking that a company with a name like Nike Deutschland would pay taxes in Germany on the profits it earns, since that’s what other companies in the German retail sector do. But that would be a little naïve.

The truth is that the brand with the swoosh is based somewhere else entirely.

The receipt for the Air Pegasus Racer shoes from the Nike store in Brunnthal provided the first indication.

Ordering online in Germany is no different. A pair of Air Pegasus Racers are easy to find on Nike.de, but when the package arrives, a note inside the box confirms that Nike Retail BV is the vendor – the same company responsible for selling swoosh-branded goods in Nike’s German stores. Sales at conventional shoe retailers and department stores – the distribution channel that industry observers say generates the most shoe sales for Nike – can also be traced back to Holland. The shops pay a Dutch company for the Nike products they sell in Germany, namely Nike European Operations Netherlands (NEON), according to sources within the industry.

The trail repeatedly leads back to the Netherlands. Reporting and test purchases by international journalists under the auspices of the International Consortium of Investigative Journalists (ICIJ) confirms this to be true for large swathes of Western Europe. Whether at Nike stores, online or at specialized retailers, customers are constantly doing business with Dutch firms – either directly or indirectly.

None of this is by chance. The Netherlands has become one of Europe's foremost tax havens, especially for American corporations. The country, one of the founding members of the European Economic Community in 1957, attracts large corporations in ways that are detrimental to its neighbors. The Netherlands doesn’t even make much money off the policy, either. It certainly isn’t receiving a significant tax-revenue boost from Nike’s profits. At best, the policy creates jobs through the many firms that run their European operations from the Netherlands. It’s a prime example of the first principle of tax havens: A little in one’s own country is better than a lot in someone else’s.

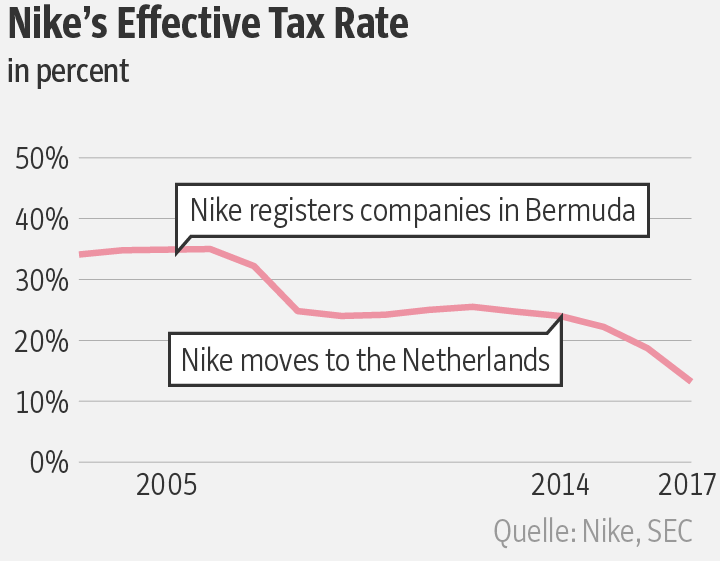

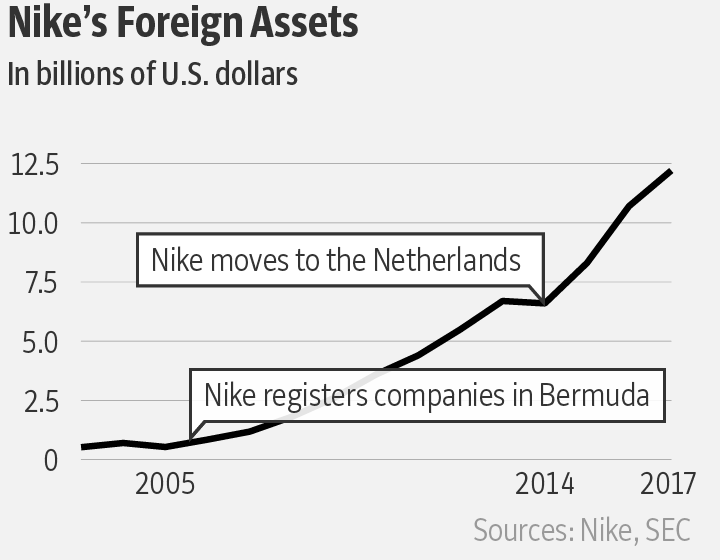

That all changed in the mid-2000s, when Nike and the law firm Appleby first implemented a tax structure that would save the sportswear-maker billions in taxes on profits generated outside the U.S. In order for the new trick to work, Nike had to move to Bermuda, a British Overseas Territory made up of coral islands that was transformed into a tax haven. To be more precise, the company moved the rights for various Nike trademarks for markets outside the U.S. Back home in America, everything stayed the same.

Bermuda is home to the Nike subsidiary Nike International Ltd, around which a network of other offshore Nike companies has been established. Most of them are named after shoes: Nike Jump, Nike Air Max or even Nike Pegasus. Their exact functions aren’t always clear, but one thing is unequivocal: Soon after the companies were founded in Bermuda, Nike subsidiaries around the world, such as those in the Netherlands, began sending them astronomical sums of money to be able to continue selling Nike shoes with the famous swoosh.

In other words, Nike pays Nike so that Nike shoes can look like Nike shoes.

That may sound strange, but it’s not. Nike’s shoe-selling Dutch conglomerate doesn’t only rake in revenues – it also racks up considerable costs.

It must pay so much to Nike International in Bermuda for the swoosh and other licenses that, at best, only diminished profits remain. In 2010, 2011 and 2012 alone, a total of $3.86 billion flowed to Nike International for use of the logo and other trademarks, according to a disclosure Nike made during a court battle with the Internal Revenue Service. Unlike Germany and most other European countries, the Netherlands does not impose a withholding tax on royalty payments. This allows money to flow unimpeded to Nike’s subsidiary in Bermuda, where, in turn, taxes are not levied on foreign profits for firms based there.

That’s why Nike chose the Netherlands. It allows the company to dodge the state.

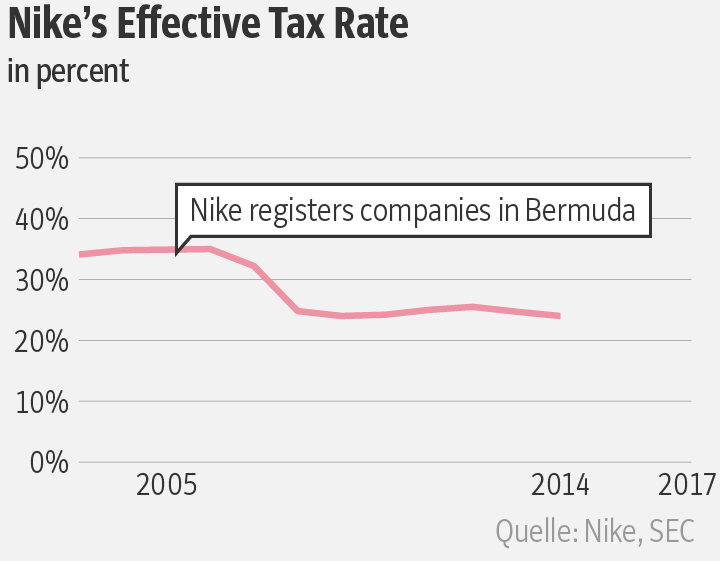

The result of Nike’s Bermuda strategy can be found in the company’s annual reports. The sporting goods manufacturer’s effective tax burden fell from a normal tax rate of 35 percent in 2005 to under 25 percent in 2008.

At the same time, Nike’s essentially tax-free profits outside the U.S. began to grow rapidly – from around $1 billion in 2005 to more than $6 billion in 2014.

In a conference call with analysts at the end of 2006, Nike CEO Mark Parker made clear how pleased he was with the situation at the time. The Securities and Exchanges Commission released a recording of the call as part of the public record. “So, how are we doing?” Parker asked, before answering, “In a word, I would say, ‘good.’” He then listed off various successes, including a long-term agreement with European tax authorities. The Nike executive said this had “secured a big advantage” for the company. In the following years, Parker would see his annual salary nearly double to $13 million by 2010.

Nike declined to comment directly on its tax strategy, telling the Süddeutsche Zeitung and ICIJ, with which this newspaper shared and jointly reviewed the Paradise Papers, only that “Nike fully complies with tax regulations,” and “we rigorously ensure our tax filings are fully aligned with how we run our business, the investments we make and the jobs we create.”

It’s no surprise that Nike comports itself in ways that conform with the law. Indeed, one of the central findings in the Paradise Papers is that multinational corporations can adhere to almost all the world’s tax regulations while still largely avoiding the need to pay taxes. All they need to do is know every trick and loophole – and always be flexible and agile.

And so it came to be that the swoosh had to move yet again.

The likeliest reason for this was the looming expiration in 2014 of the aforementioned tax agreement – the one praised so strongly by Nike’s CEO – between the company and the Netherlands. That deal had also apparently stipulated that licensing royalties could flow onward to Bermuda. A solution had to be found, and surprisingly it resulted in Nike relying less on Bermuda and more on the Netherlands for its European business. The Paradise Papers show how Nike dissolved numerous companies in Bermuda and transferred their shares to firms in Holland. During that time, Appleby billed Nike for the registration, relocation and deregistration of various companies, all of which were listed under the category “restructuring.”

From that point on, a Dutch firm called Nike Innovate CV owned the rights to hundreds of Nike brands. In the World Intellectual Property Organization’s Global Brand Database, some 2,000 brands and patents are registered to the company. Other Nike subsidiaries evidently directed payments to Nike Innovate CV’s accounts for the right to use the name Nike, the swoosh logo and other product designations. In the past two years, those payments added up to 1 billion euros a year.

Nike Innovate CV, for its part, is a rather unique organization. In Dutch, it’s called a commanditaire vennootschap – hence the abbreviation CV – a form of limited partnership. CVs are unusual company structures in the Netherlands that create differing tax treatments and can help multinationals escape big tax bills. Technically, the company’s headquarters is in the U.S., but from a tax perspective, Nike Innovate CV is essentially stateless.

For an outsider, the utility of having so many CVs is not immediately clear. It may simply be an effort to make the entire arrangement less visible. It’s also unclear in which of these CVs the billions in licensing royalties are parked. But that’s not the point. What’s important is that the Dutch authorities don’t feel responsible for taxing Nike because CVs aren’t taxed in the Netherlands. The Americans, on the other hand, see a subsidiary of a U.S. company and believe it’s the Dutch CV that should be paying taxes – in Holland.

The U.S. points a finger at the Netherlands, which points a finger back at the U.S. Both countries refuse to collect taxes – and in the end, Nike wins. By moving the holder of Nike’s many trademarks from Bermuda to the Netherlands, Nike was able to lower its effective tax rate to an astounding 13.2 percent in 2017.

One of the reasons this rate is so low is because Nike was able to secure some one-off tax discounts following a dispute with U.S. tax authorities. In an outlook for 2018, Nike CEO Parker said the company would face a global tax rate of 15 to 17 percent – considerably less than what such a large company would normally owe in the U.S. or Germany.

Former U.S. Senator Carl Levin once referred to complex networks of companies that in the end aren’t taxed anywhere as the “Holy Grail of tax avoidance.” He was referring to the tech giant Apple at the time, but his words could apply to most international corporations today. The Nikes of the world move around the globe, planting their flag in one tax haven after another. They can be found almost anywhere, yet they are taxed virtually nowhere.

For American companies, the Netherlands has become the most important tax haven in the world. Not Bermuda, not the Cayman Islands, not Panama – the Netherlands, smack dab in the middle of the European Union. In addition to Nike, the Paradise Papers also contain information on the ride-hailing service Uber, the electric carmaker Tesla and the office supply company Office Depot, all of which use the Dutch tax loophole. There are other companies too that don’t show up in the Paradise Papers but also embrace Holland’s favorable tax policies, including the media company CBS, the delivery service FedEx, the pharmaceuticals giant Pfizer and others. In all, there are more than 150 CV-BV constellations used by American multinationals listed in the Netherlands' company register. BV stands for besloten venootschaap, a limited liability company the shell firm sets up as a subsidiary.

Experts have criticized the CV-BV model for years, going so far as to accuse the Dutch government of violating competition laws by providing companies with illegal state subsidies. Amsterdam has yielded some by announcing it would change the law, but it has reached an agreement with the EU to keep the loophole open until 2020.

For the most part, Germany has remained quiet about the practices of its neighbor to the west. This is rather surprising considering the German tax office only sees a small portion of what Nike earns in the country each year. Nike reports sales in Western Europe of around 6 billion euros annually, much of which come from Germany, Western Europe’s most important sporting goods market. Industry insiders with intimate knowledge of sales figures say Nike sells around 600 million euros worth of merchandise in Germany alone. But according to the German commercial register, Nike Deutschland GmbH’s sales revenues in Germany were only about 76 million euros in 2016. Of that, the state received around 3.8 million euros in taxes, a little more than a half a percent of Nike's probable revenues in this country.

Moving the “swoosh” and Nike’s other trademarks from the U.S. to Bermuda, and then from Bermuda to the Netherlands, has led to a situation in which Nike has amassed enormous foreign assets. By May of this year, that figure had reached more than $12 billion. “This makes it clear that the company has paid virtually no income tax” on those profits, Matt Gardner, a tax expert with the Tax Justice Network, said after reviewing Nike’s 2017 annual report.